Global downturn hitting the Swiss economy

- KOF Bulletin

- KOF Economic Forecasts

The signals coming from the Swiss economy have deteriorated recently. Industry, for example, is reporting a decline in capacity utilisation. The international environment has also changed. Forecasts for the global economy have become less upbeat. Weaker international business activity and the recent appreciation of the Swiss franc will have consequences. KOF is therefore lowering its forecast for economic growth this year and next.

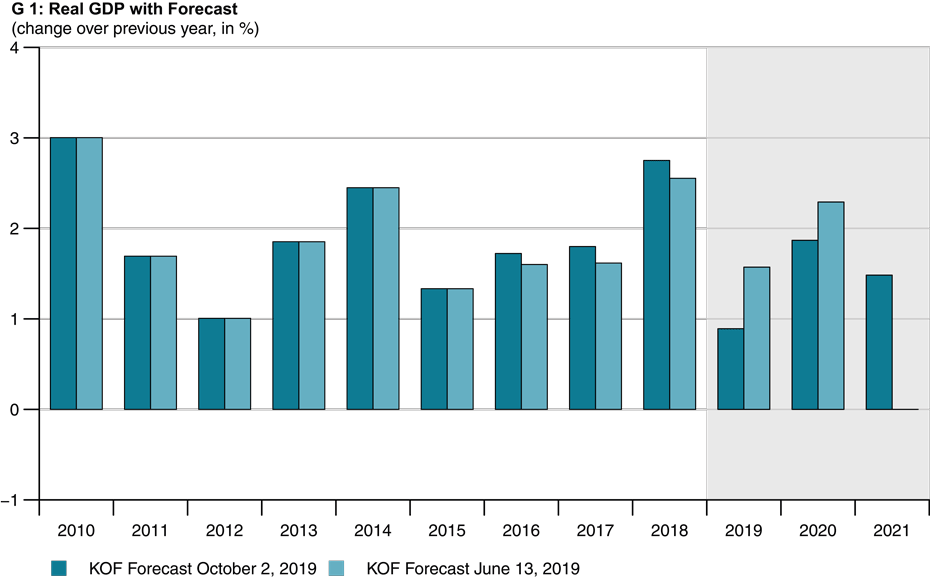

Growth in gross domestic product (GDP) will be slightly weaker than the numbers suggested in the spring. The slowdown in international business activity and the economic data published for the first half of 2019 have prompted KOF to lower its forecast for economic growth in 2019 from 1.6 per cent to 0.9 per cent (1.4 per cent excluding sporting events). It has also revised downwards its forecast for 2020 – from 2.3 per cent to 1.9 per cent (1.5 per cent excluding sporting events). KOF expects to see growth of 1.5 per cent in 2021 (1.8 per cent excluding sporting events).

The international environment for the Swiss economy has continued to deteriorate in recent months. Business activity in the euro area slowed in the second quarter of 2019 and global trade contracted sharply – following what had already been two negative quarters. The trade dispute between the United States and China continues to escalate. The US plan to take further protectionist measures against the European Union (EU) could soon become reality. The threat of tariffs on cars remains particularly acute.

Although Switzerland would only be indirectly affected by these measures, suppliers of components for car production could be hit especially hard. Further sharp economic downturns suffered by Switzerland’s trading partners would have an adverse impact on most exporters in this country.

Some areas of industry must expect setbacks

The continuing high level of uncertainty, the sluggish international economy and the recent appreciation of the Swiss franc will have a negative impact on large sections of Swiss industry. The engineering sector, for example, will need to brace itself for further setbacks. Its volume of new orders has been disappointing for some time now. The stronger Swiss franc will also act as a drag on the tourism sector, which is usually affected by exchange-rate movements.

The pharmaceutical industry, which accounts for the largest share of Swiss exports, is traditionally largely immune to fluctuations in the economic cycle. However, it will see its profit margins narrow temporarily because the prices at which medicines are sold in many countries are set by the government. It is therefore not possible to adjust these prices briefly in response to the appreciation of the Swiss franc.

Unemployment rate set to rise gradually

Weaker economic growth will cause employment to increase more slowly, which will have a corresponding impact on unemployment. KOF expects the unemployment rate to rise modestly instead of continuing to fall.

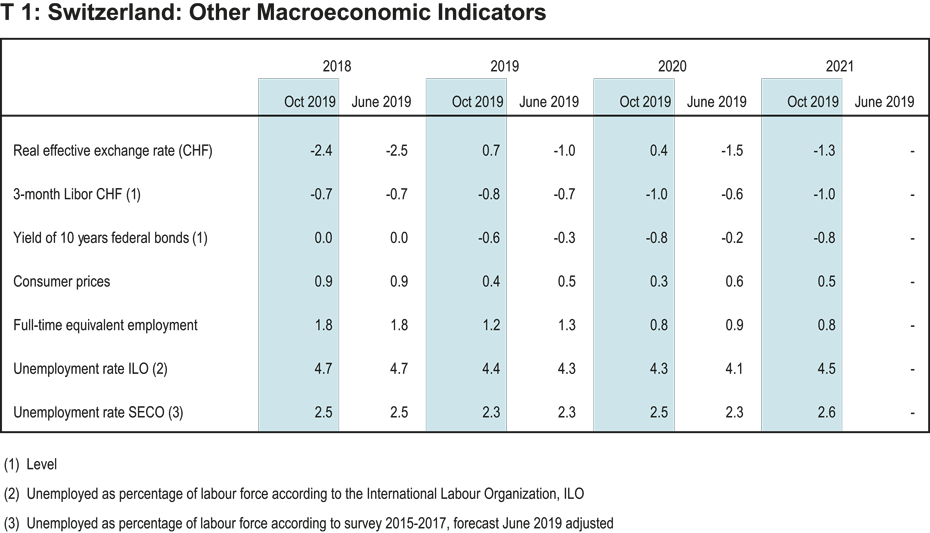

Wage growth remains subdued as well. However, pay settlements are expected to be slightly higher than in recent years. Because inflation is set to remain very low, this will result in modest but positive real wage growth.

Number of housing starts decreasing slowly

The construction sector has acted as a key stabiliser in recent years. It will continue to perform this role, albeit to a lesser extent. Although the civil engineering and commercial construction sectors remain buoyant, KOF is fairly sceptical in its forecast for residential construction. The number of housing starts over the past few years has been higher than the increase in the number of households. Despite record-low mortgage interest rates KOF expects new construction in this segment to decline gradually.

The situation looks slightly better with respect to trade. Although the stronger Swiss franc could boost shopping tourism, this is not expected to rise sharply. Uncertainty about oil production in the Middle East going forward as well as the ongoing international trade conflicts are fuelling greater volatility in commodity prices. This is having an adverse impact on manufacturing.

Further interest-rate cuts to come

The European and American central banks have both loosened monetary policy in order to curb any further slowdown in economic activity. Such developments generally boost demand for safe investments, which traditionally include the Swiss franc. Against this backdrop the franc’s recent appreciation comes as no surprise.

The Swiss National Bank (SNB) expanded its foreign-exchange reserves during the summer. In addition, it recently significantly raised the allowances available for the sight deposits held at the SNB. The latter measure would enable it to cut its negative interest rate further without increasing the burden on those financial institutions with deposits at the SNB compared with recent years. KOF expects the upward pressure on the Swiss franc to continue – partly because a further modest rate cut by the European Central Bank is anticipated. The SNB will therefore lower its interest rates towards the end of the year.

Forecasting risks

The greatest economic risks to Switzerland continue to come from abroad. A potential escalation of the ongoing trade conflicts or any other disruption might cause the Swiss franc to appreciate further, which would be bad news for exporters. KOF expects the United Kingdom’s exit from the EU to be delayed until at least the end of January 2020. If – contrary to this assumption – a no-deal Brexit happens by 31 October this year, the associated disruption is likely to cause more harm to the European and Swiss economies than has been suggested in this forecast.

An Executive Summary of the Economic Forecast can be found Download here.